Streaming media is the new style of watching TV. Around the world, more and more people are bypassing traditional sources of media, like cable television, to stream series, shows and live events via the internet. With over-the-top (OTT) platforms surging in both subscribers and engagement, OTT is quickly becoming a key vertical for mobile marketers.

CTV, OTT and “Cord-Cutting”

A Connected TV (CTV) is a device that facilitates the delivery of streaming video content. Some of these devices include Xbox, PlayStation, Roku, Amazon Fire TV, Apple TV and Chromecast.

OTT is the delivery of TV content via the internet. This content is accessible outside of traditional cable or satellite provider subscriptions. Popular OTT services include Netflix, Hulu, and Amazon Prime. Mass media and entertainment have also launched their own OTT services such as Disney+ and NBC’s Peacock.

The rise of CTV and OTT has led to the phenomenon of “cord-cutting”. This refers to the growing trend of consumers canceling their traditional cable subscriptions in favor of streaming services. In 2020, 80% of consumers streamed content using CTV.

Putting this all together, OTT describes any gadget or service used to stream digital content to a TV or similar device. Some common OTT platforms include:

- Game consoles

- Smart TV

- Streaming Boxes (Samsung Allshare Cast, Amazon Fire TV, Apple TV)

- Internet-enabled smart blu-ray/DVD players

- HDMI sticks (Amazon Fire TV Stick, Chromecast, Roku)

- Mobile Devices via in-TV apps like HBO Go and Netflix

The OTT Opportunity

Revenue in the video streaming segment is expected to grow to $30.4 billion by 2024. This growth means that OTT advertising will also rise, as marketers maximize the growing OTT audience opportunity.

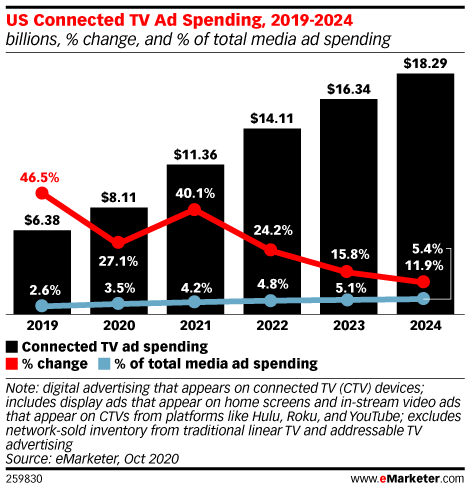

In 2020, US CTV ad spend totaled $8.11 billion. Spend will increase to $11.36 billion by the end of 2021. By 2024, spend will reach $18.29 billion.

Source: eMarketer

Mobile is an important and growing component of the OTT landscape. According to video analytics company, Conviva, CTV viewing on mobile devices was up 13% between February and March 2020.

In 2020, 75% of people watch premium video on their mobile devices at least monthly and 40% of people do so daily. Although young people are the most prolific mobile streamers, older age groups are growing in the mobile streaming segment. For example, half of people 45 to 50 years old streamed via mobile devices in 2020 at least weekly, and 30% watched daily.

Mobile Attribution and OTT

OTT is on the rise, and subsequently, so is OTT advertising. How do advertisers understand if their OTT ads directly impact their ROI? Here’s where the mobile ecosystem is currently at in terms of attributing OTT ad spend to mobile acquisition goals.

The OTT Attribution Challenge

The attribution challenge on OTT is a big one to say the least. Given the multi-device nature of OTT, attribution will need to have cross-device measurement capabilities. In an ideal world, OTT attribution would link CTVs and mobile devices since a viewer might see an ad for an app on a CTV and then take an action on their mobile device. However, effectively creating a direct link between those two device types is hard.

Traditional TV advertising measurement is done through probabilistic attribution. TV advertisers receive standard reporting on estimated impression delivery by demographic based on TV ratings and Nielsen panel data. They then compare whether the group of people exposed to an ad bought more products compared to the group of people who were not exposed to the ad. For now, attribution from CTV ads to mobile devices relies on the same probabilistic methodology as traditional TV.

Cross-device attribution has also become even harder in the face of consumer data privacy changes. Mobile advertisers need to gain user consent to measure the impact of their ads starting in early spring. That means there is no easy way out of the OTT attribution challenge by passing around user IDs.

Solutions

Many consumers use mobile phones for OTT streaming. In this scenario, marketers can measure mobile ads like for any other ad on mobile devices. Most MMPs offer deterministic attribution of OTT app downloads occurring on the same platform as a CTV ad.

That said, some marketing cloud companies have offered “identity graphs” that use household and user-based signals to provide advanced cross-device attribution from CTV, but these offerings are not currently integrated with any major MMP.

The IAB Tech Lab is in the process of building the OTT IFA, which is the OTT version of the soon-to-be restricted IDFA. The OTT IFA is a protocol that allows for data standardization and campaign measurement. The more OTT services, marketers and intermediaries start applying this protocol, the more effective measurement will become.

Above all, OTT measurement will require collaboration. Players need to develop a narrative that explains why ad impact measurement is vital for OTT services, not just for marketers' benefit but for consumers as well.

What This Means for Mobile

OTT user adoption was growing before the pandemic hit, but the trend has accelerated mightily over the past year as entertainment-hungry viewers are relegated to their homes. To maximize the growing OTT opportunity, players are jockeying into position. News broke today that Magnite acquired video supply-side platform SpotX from European entertainment network RTL Group for $1.17 billion. This is more than four times the amount RTL originally paid to acquire the company, showing just how hot the CTV market is becoming. This acquisition is just one example of major players investing more in the OTT space.

Apple’s planned restrictions of the IDFA also makes the CTV and OTT more attractive. Marketers can still use high-level user targeting in the CTV/OTT space, where you can still target your ads on a household or individual level.

Now is the time for marketers to invest in CTV and OTT partners that can provide sophisticated audience targeting solutions to the cross-device attribution challenge. For example, cable and OTT providers can tie their subscriber data to first- and third-party data using email address or device IDs.

For IDFA-dependent marketers, the IDFV could be an alternative unique ID for each customer. Of course, the average consumer has about 20 to 25 apps on their iPhone so there will be 20-25 unique identifiers depending. Then tying those IDs to an individual through email addresses could be an option of tracking them outside of app interactions. (Although this could pose its own challenges as the average customer has multiple emails.) The key is to work with a TV identity partner that can connect IDs across multiple touch points at the household level so that marketers can create a single identity for their customers across multiple screens.

Takeaways

Overall, CTV measurement is still extremely fragmented, much like the wild west of mobile attribution a decade ago. However, the high growth rate of OTT will naturally lend itself to technical advancement over time. Moreover, the synergies between OTT apps and mobile present clear opportunities for app marketers to start testing OTT platforms sooner than later.

- CTV: a device that facilitates the delivery of streaming video content.

- OTT: the delivery of TV content via the internet.

- Given the multi-device nature of OTT, attribution will need to have cross-device measurement capabilities.

- While OTT streamed on mobile devices can be attributed deterministically, attribution from CTV ads to mobile devices relies on the same probabilistic methodology as traditional TV.

- It’s vital that players collaborate to develop a narrative explaining why ad impact measurement is vital to OTT services and providing consumers with a unique ad experience.